Zopa has officially launched its new Biscuit current account, offering 2% cashback on bills and a market-leading 7.1% regular saver—but does it live up to the hype?

Zopa Biscuit Current Account: Key Features

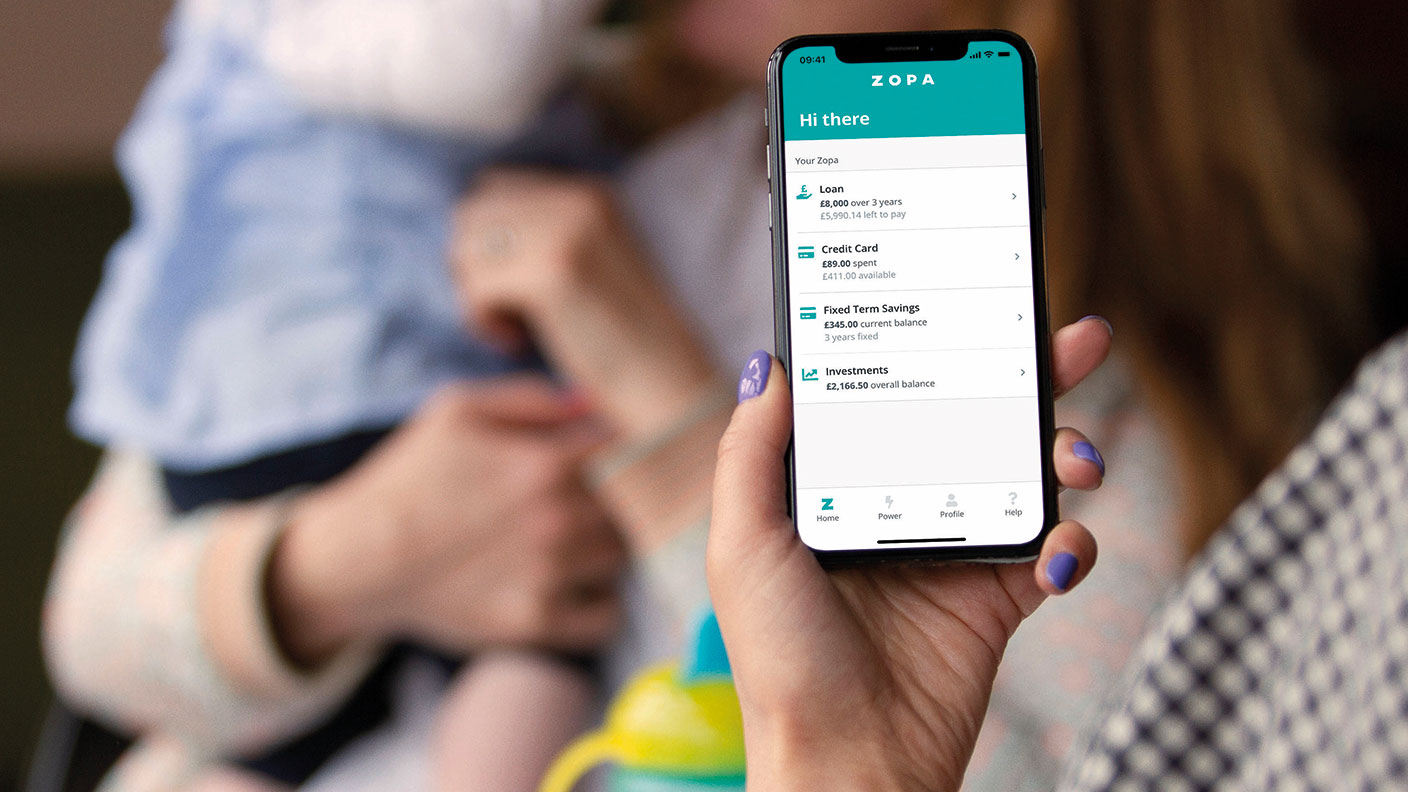

The digital-only account is free to open and managed entirely via the Zopa app. Here’s what’s on offer:

✔ 2% cashback on direct debits (capped at £1,500/year = max £30/year)

✔ 7.1% variable-rate regular saver (up to £300/month, potential £137/year)

✔ No fees for spending abroad

✔ Interest on balances (though rates are low compared to top savings accounts)

How Does the Cashback Compare?

While 2% cashback sounds appealing, the £30/year cap makes it far less competitive than alternatives:

-

Chase UK – Still offers uncapped 1% cashback on everyday spending.

-

Trading 212 debit card – 1% cashback with no direct debit restrictions.

-

Santander Edge – Discontinuing its 1% cashback offer in September.

The Big Draw: 7.1% Regular Saver

The standout feature is the 7.1% variable-rate savings account, currently the best 1-year regular saver available.

-

Save up to £300/month (£3,600/year).

-

Potential £137 interest (if the rate stays unchanged).

How it compares to rivals:

| Provider | Rate | Term | Monthly Limit |

|---|---|---|---|

| Zopa | 7.1% (variable) | 1 year | £300 |

| First Direct | 7% (fixed) | 1 year | £300 |

| Co-op Bank | 7% (variable) | 1 year | £250 |

| Principality | 7.5% (fixed) | 6 months | £250 |

Best alternative? First Direct’s fixed 7% rate may be safer than Zopa’s variable offer.

Verdict: Should You Switch?

✅ Good for: Savers wanting a high-yield regular saver and minimal foreign fees.

❌ Not the best for: Cashback seekers (due to the low cap) or those wanting top-tier interest on balances.

Final thought: While Zopa’s 7.1% saver is compelling, the cashback is underwhelming. If you’re after better rewards, Chase or Trading 212 may be smarter choices.